- The Andorran banking model consolidates its position with sustained growth in profits (+1%), client assets under management (+21%) and deposits (+6%), remaining diversified and profitable, with a ROE of 9,5%

- Key ratios such as solvency and liquidity remain above the European banking average, reinforcing the sector’s competitive strength and resilience

- Domestic lending increased by 10%, while the non-performing loan ratio fell to a historic low of 1.5%

The Andorran banking sector closed the 2025 financial year with a consolidated profit of 176 million euros, representing a 1% increase compared with the previous year. This performance reflects an environment marked by the normalisation of interest rates, which has placed some pressure on financial income, offset by the business model’s ability to adapt to new market conditions and evolving client needs.

Total client assets managed by banking institutions — including deposits, investment funds and discretionary mandates — reached €113.248 million, up 21% compared with 2024, while deposits increased by 6%. This trend highlights the Andorran financial centre’s strong ability to attract and retain capital.

A profitable, diversified and sustainable model

The Andorran banking business model remains solid and diversified, combining retail and private banking activities with an international presence, enabling institutions to adapt to a changing financial environment.

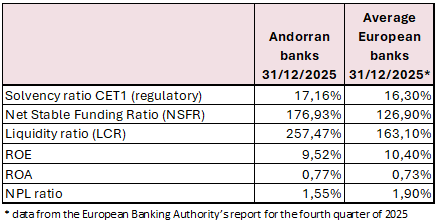

Banks achieved a return on equity (ROE) of 9.52%, in line with the European average. Return on assets (ROA) stood at 0.77%, remaining above the European average. This was achieved in a context of progressive interest rate stabilisation, which institutions have managed effectively.

Structural strength: solvency and liquidity above European standards

The figures confirm the strength of the Andorran financial system. As of 31 December 2025, the CET1 capital ratio stood at 17.16%, slightly above the European average (16.3%). The liquidity coverage ratio (LCR) reached 257%, well above both the regulatory minimum of 100% and the European average (163%).

In addition, the net stable funding ratio (NSFR), which measures the long-term stability of banks’ funding, stood at 177%, clearly above the European banking average of 126% and 8 percentage points higher than in 2024. This reflects the ability of Andorran institutions to maintain structurally sound and stable long-term funding.

Likewise, the non-performing loan (NPL) ratio declined once again to a historic low of 1.5%, supported by prudent credit underwriting and risk monitoring policies, as well as the positive performance of the Andorran economy. The European average NPL ratio stands at 1.8%.

Commitment to the country’s economic growth

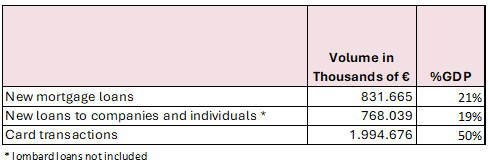

Total lending in the domestic market reached €5.561 million in 2025, representing a 10% increase year-on-year. This financing volume accounts for 140% of GDP, a high level compared with peer economies, underscoring the importance of credit in financing economic activity and the central role of the banking sector in financial intermediation.

In this context, the sector channelled €1.599 million in new financing, equivalent to nearly 40% of GDP. A total of 1,064 new mortgages (+38%) were formalised, amounting to €831 million, while €768 million in loans to businesses and households (+20%) were granted. This momentum is partly explained by the stabilisation of financial conditions and the dynamism of the real estate and business sectors.

At the same time, card payment volumes increased to €1.994 million (+11%), reaching 50% of GDP, in line with solid demand and a high level of economic activity.

A sector recognised for its stability and competitiveness

The International Monetary Fund highlights the important role of Andorra’s financial system, which represents the country’s fourth-largest economic sector. The international institution underscores the diversification of the business model, with a balanced mix of retail and private banking, and recognises the sector’s resilience under adverse scenarios.

According to Esther Puigcercós, CEO of Andorran Banking:

“Andorran institutions maintain a solid capital position and liquidity levels above the European average, reinforcing the resilience of the system in changing economic environments. Having a robust and well-capitalised banking sector is essential to boosting the country’s competitiveness and ensuring continued support for the growth of the Andorran economy.”

These figures correspond to a preliminary update of the official year-end results as of 31 December 2025 and remain subject to review and approval by auditors and the relevant governing bodies.